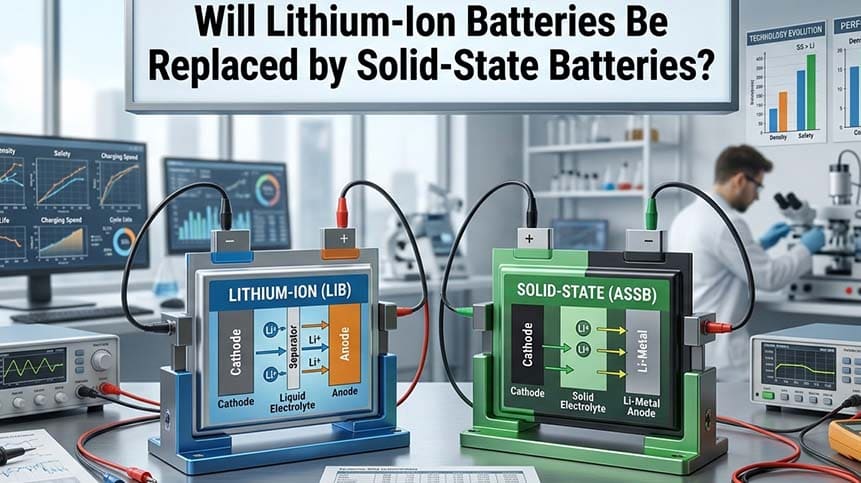

As technical directors and battery manufacturing experts navigating the rapid evolution of global energy storage, we are frequently asked a critical question by B2B clients and automotive innovators alike: Will solid-state batteries completely replace traditional lithium-ion batteries?

Based on current industry research, production telemetry, and expert consensus in 2026, our short answer is no, not completely.

While all-solid-state batteries (ASSBs) undoubtedly represent the next frontier of high-density energy storage, they will not trigger the total obsolescence of liquid electrolyte systems. Instead, the industry is moving toward a diversified paradigm where liquid, semi-solid (mixed solid-liquid), and all-solid-state batteries will coexist for decades. Below, I provide a detailed, data-driven breakdown of the manufacturing, economic, and chemical realities defining this technical trajectory.

1. The Realities of the Commercialization Timeline

A common misconception fueled by mainstream tech headlines is that solid-state batteries are ready to take over the mass market immediately. However, looking at actual factory floor readiness reveals a highly fragmented timeline.

While 2026 is highlighted as the "first year of mass production" for certain solid-state configurations, this milestone refers strictly to small-scale, high-cost prototype runs and premium demonstration models. Leading battery tech figures, such as Xu Hangyu (Technical Director at Weilan New Energy/WeLion), openly state that true commercialization—characterized by high-volume, cost-effective mass production—is highly unlikely to materialize until after 2030.

Solid-State Battery Commercialization Roadmap:

[2026] --------> Small-scale premium prototype runs / specialized applications

[2027-2028] ---> Small-volume EV demonstration fleets (CATL, BYD, Toyota pilot models)

[2030+] -------> True large-scale commercialization and cost-competitive scaling

Global manufacturing giants are pacing themselves carefully. Companies like CATL and BYD have targeted 2027 for small-volume deployments in luxury or niche electric vehicle models. In stark contrast, the classic lithium-ion battery infrastructure is exceptionally mature. Backed by highly optimized global supply chains, the lithium-ion market is structurally secure, with its global market valuation projected to climb to USD 248.6 billion by 2035. Replicating this scale of gigafactory infrastructure for a completely new chemistry cannot happen overnight.

2. The Prohibitive Cost Barrier: A Quantitative Breakdown

The single most rigid barrier to the widespread adoption of solid-state technology is its substantial cost disadvantage. To put this in perspective, we have compiled a 2026 engineering cost comparison analyzing the manufacturing expense per kilowatt-hour (kWh) across different battery architectures.

| Battery Technology Profile | Average Manufacturing Cost (per kWh) | Energy Density (Wh/kg) | Primary Market Segment (2026–2035) |

|---|---|---|---|

| Lithium Iron Phosphate (LiFePO4 / LFP) | $60 – $75 | 160 – 200 Wh/kg | Mass-market EVs, Stationary ESS, Telecom Backups |

| Nickel Manganese Cobalt (NMC) | $85 – $110 | 230 – 300 Wh/kg | Mid-to-High Performance EVs, Consumer Electronics |

| Semi-Solid State Batteries | $140 – $180 | 300 – 380 Wh/kg | Premium EVs, Performance Industrial Drones |

| All-Solid-State Batteries (ASSB) | $220 – $350+ | 400 – 500+ Wh/kg | Luxury EVs, Aerospace/eVTOL, High-End Medical |

To understand what this means for a standard vehicle layout: provisioning a standard 70 kWh battery pack for a mass-market electric car using all-solid-state cells instead of LFP technology would add over $11,000 USD in raw manufacturing costs alone.

This severe pricing premium stems from two core challenges:

Expensive Raw Material Synthetics: Solid electrolytes require complex, high-purity inputs like lithium sulfide or advanced ceramic oxides, which do not yet benefit from high-volume economies of scale.

Incompatible Tooling Lines: Solid-state batteries cannot be built on existing liquid-coating production lines. They require brand-new, ultra-high-precision manufacturing equipment operating under extreme dry-room environments to handle delicate solid-electrolyte interfaces.

For cost-sensitive applications like affordable commuter cars and grid-scale energy storage systems (ESS), liquid-electrolyte lithium-ion batteries will remain the undisputed dominant choice for the foreseeable future.

3. A Future of Market Coexistence and Technical Succession

Rather than a "winner-takes-all" scenario, the future energy storage landscape will split into clear, highly specialized market segments. Each technology will play to its unique physical and economic strengths.

Liquid Lithium-Ion Batteries (LFP/NMC): The Mass-Market Workhorses

Liquid chemistries will continue to anchor the volume tier of the global economy. Their core advantages—a fully amortized supply chain, mature recycling loops, and exceptionally low production costs—make them virtually impossible to displace in standard consumer segments. Furthermore, liquid batteries are not standing still. The continuous evolution of ultra-fast charging capabilities (such as next-generation flash-charging systems developed by top-tier suppliers) ensures that liquid packs comfortably exceed the daily range and convenience needs of 90% of global end-users.

Solid-State Batteries: The Premium Performance Champions

Solid-state cells will carve out a dominant position in high-tier applications where energy density and safety take absolute precedence over capital cost. Their unique advantages include:

Unmatched Energy Density: Achieving 400 to 500+ Wh/kg allows for dramatically lighter packs and extended runtimes.

Superior Thermal Safety: Eliminating volatile liquid organic electrolytes drastically reduces the risk of thermal runaway.

Broad Operational Envelopes: Enhanced molecular stability across extreme hot and cold ambient temperatures.

These performance metrics make solid-state technology the perfect match for luxury electric vehicles, electric vertical takeoff and landing aircraft (eVTOL / electric aviation), critical high-reliability medical hardware, and specialized military applications.

As Weilan New Energy's technical director, Xu Hangyu, precisely summarized: "The future technical landscape will very likely be the long-term coexistence of liquid, mixed solid-liquid, and all-solid-state batteries. The three types of technology will establish their own differentiated advantages in different application scenarios."

4. Quality Standards & Sourcing Guide for B2B Operations

If your engineering team is evaluating long-term power solutions, selecting a manufacturing partner requires strict compliance with international safety and performance baselines. For specialized custom designs, check our dedicated B2B Custom Lithium Battery Manufacturing page to review our engineering workflows and explore tailormade options.

When sourcing high-capacity energy solutions, ensure your supplier provides verified documentation for the following international certifications:

IEC 62133-2 & UN38.3: Vital for ensuring cell-level structural integrity during high-vibration international logistics and operation. You can cross-verify compliance criteria via the official International Electrotechnical Commission (IEC) portal.

UL 1973 / UL 9540A: Crucial safety benchmarks for stationary battery architectures and grid deployments. For updates on regional deployment regulations and evolving grid standards, consult the Solar Energy Industries Association (SEIA) industry database.

5. Frequently Asked Questions (FAQ)

Q1: Why can't solid-state batteries be manufactured on existing lithium-ion production lines?

A: Liquid lithium-ion batteries rely on automated slot-die coating processes to flood porous separators with liquid electrolyte. Solid-state batteries require completely dry processing or high-pressure powder compaction to create a seamless, solid-to-solid contact interface between the electrodes and the solid electrolyte layer. This demands an entirely different generation of high-precision manufacturing equipment and highly controlled ambient environments.

Q2: What exactly is a semi-solid-state battery, and how does it bridge the gap?

A: A semi-solid-state (or mixed solid-liquid) battery retains a small percentage of liquid electrolyte (typically 5% to 10% by weight) within a solid matrix or polymer gel network. This hybrid design enhances safety and boosts energy density beyond standard liquid cells, while still allowing manufacturers to use a significant portion of their existing liquid assembly lines—acting as an affordable stepping stone toward true all-solid-state production.

Q3: Will solid-state technology eventually make lithium-ion battery recycling obsolete?

A: No. All-solid-state batteries still utilize valuable critical materials such as lithium, cobalt, nickel, and manganese within their cathode structures. While the solid electrolyte itself changes the mechanical disassembly process at recycling facilities, the fundamental hydrometallurgical and pyrometallurgical processes used to extract and reuse these valuable metals will remain highly relevant.